Executive Summary

- The market is real, but expectations are still creating a valuation debate. The agentic AI market reached $7–7.5 billion in 2025 and is forecast to grow to $57–199 billion by 2031–2034. However, significant methodological inconsistencies exist across estimates — investors should read these projections with caution.

- Enterprise adoption is fast but shallow. Google Cloud research shows 52% of executives say their organizations have deployed AI agents. McKinsey finds 62% of organizations are still in "experimentation" mode. Deep production deployment remains limited to a selective minority.

- First real revenue signals are arriving. Salesforce Agentforce reached $540M ARR within a few quarters. GitHub Copilot surpassed 20 million users. Cursor achieved $1B ARR in 24 months. These are concrete commercial proofs.

- Infrastructure transformation is the clearest winner. Nvidia data center revenue grew 93% YoY. AWS Bedrock customer spend increased 60% in a single quarter. Arista Networks announced a $105B AI networking TAM. Money flows in this layer are the most tangible.

- SaaS business models are under pressure. Per-seat pricing is facing a structural crisis. Salesforce, Adobe, and Atlassian shares fell 26%, 19%, and 30% respectively in 2025. The "SaaSpocalypse" is real but its timing is overstated.

- Gartner issued a critical warning. More than 40% of enterprise AI agent projects will be canceled by 2027. As of 2025, only ~130 providers are genuinely considered "agentic" — the rest are rebranded chatbots or RPA.

- The real bottleneck is not the model, it's integration. Legacy system integration, data quality, and security stand out as the biggest barriers to enterprise deployment. The technology is ready; organizations are not.

- Value is accumulating most in infrastructure, then platform layers. Application software companies are caught between two fires: building AI to avoid losing their customers while simultaneously putting their own revenue at risk.

1. Conceptual Framework: What Is an AI Agent?

The Terminology Confusion — and Why It Matters

The term "AI agent" is used in at least five different ways in the market. This confusion complicates both investor analysis and product evaluation.

Term | Characteristics | Examples | Autonomy Level |

|---|---|---|---|

Chatbot / Assistant | Q&A, single-step, no human approval needed Get the signal, not the noise Receive concise weekly market intelligence, major narrative shifts, and new research drops. No spam. Unsubscribe anytime. | ChatGPT, basic Gemini | Low (L1) |

Copilot | Offers suggestions, human applies; code completion | GitHub Copilot, M365 Copilot | Low-Medium (L1-L2) |

Workflow Automation | Rules-based, trigger-driven automation | Zapier, Make, n8n | Medium (L2) |

AI Agent | Multi-step planning, tool use, feedback loops, memory | Salesforce Agentforce, OpenAI Codex | Medium-High (L3-L4) |

Autonomous / Agentic AI | Long-horizon goals, multi-system access, minimal human intervention | Multi-agent systems, experimental deployments | High (L4-L5) |

Companies claiming "AI agent" do not mean the same thing. According to Gartner, while there are roughly 130 legitimate agentic providers in the market, the vast majority are simply rebranded chatbots or RPA. This "agent washing" problem makes narrative analysis essential.

Why It Surged Now

Three core reasons explain why AI agents entered the mainstream so rapidly in 2024–2025: (1) GPT-4 and its successors made multi-step reasoning viable; (2) tool-use and function-calling capabilities matured significantly; (3) massive launch campaigns from OpenAI, Anthropic, Google, and Microsoft pushed "agent" discourse into center stage. However, this narrative velocity far outpaces actual production deployment readiness.

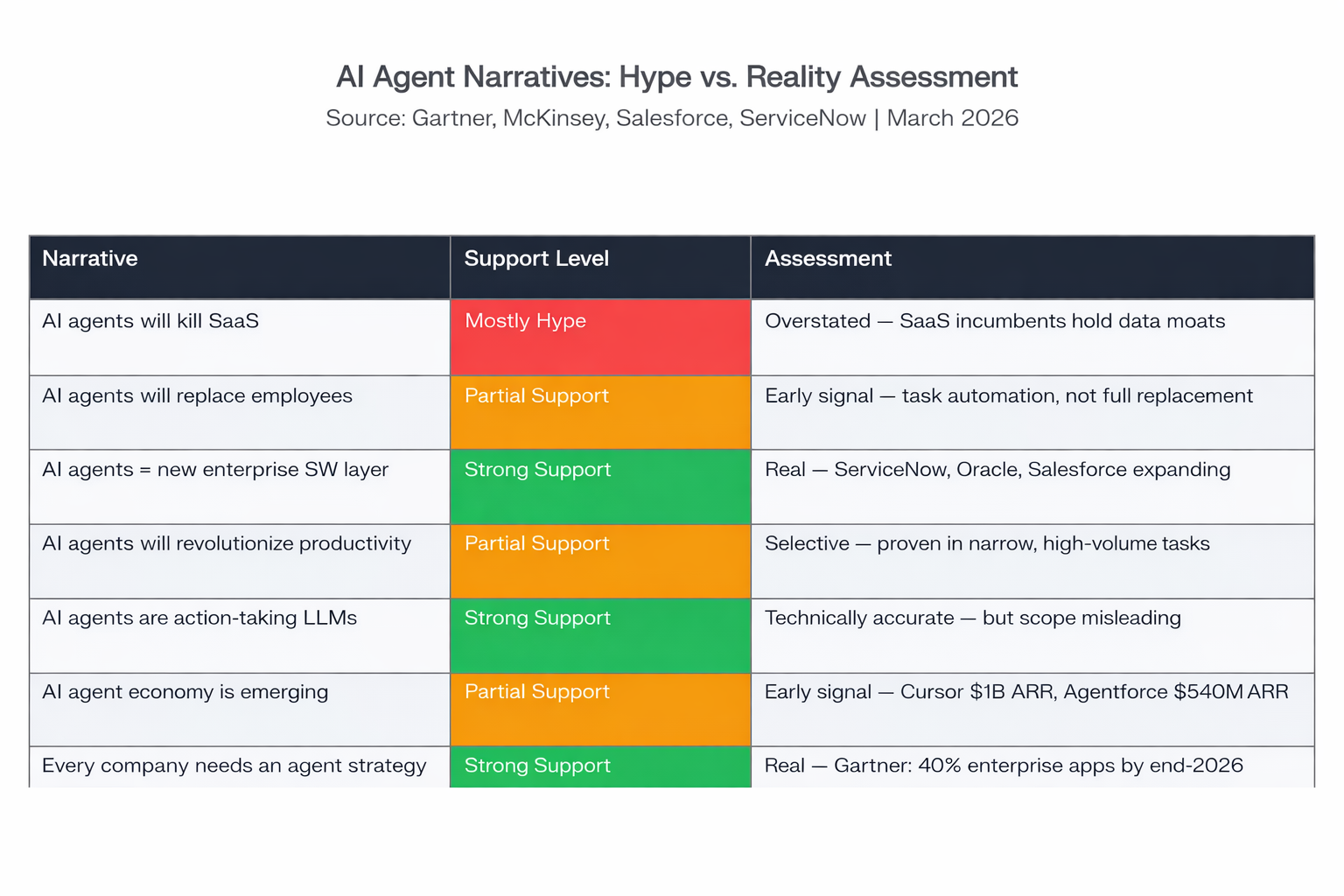

2. Dominant Market Narratives: Assessment Table

Narrative | Support Level | Assessment | Note |

|---|---|---|---|

"AI agents will kill SaaS" | Mostly Hype | Overstated | OpenAI's $280B by 2030 claim is not credible; SaaS infrastructure (Jira, Adobe, Slack) is not just UI — it is proprietary data and workflow silos. Bain Consulting holds a similar view. |

"AI agents will replace workers" | Partial Support | Early signal | Concrete productivity evidence exists in specific tasks (code review, customer query routing). But in enterprise context, "task automation" is the right framing — not full replacement. |

"AI agents = new enterprise SW layer" | Strong Support | Real enterprise adoption | ServiceNow, Salesforce, and Oracle platform expansions point this way. ServiceNow launched 1,000+ pre-built agents. Oracle added 100+ agents to its AI Agent Marketplace. |

"AI agents will revolutionize productivity" | Partial Support | Early-stage, selective proof | ServiceNow reports 20% productivity gains in its own operations, creating 3M hours of capacity. But this is a specific scenario from their own product — too early to generalize. |

"AI agents are action-taking LLMs" | Strong Support | Technically accurate | Accepted as a descriptive framework, but "action" scope remains blurry. Multi-agent systems increase token consumption 20–30x. |

"AI agent economy is emerging" | Partial Support | Early signal | Cursor's $1B ARR and Salesforce Agentforce's $540M ARRdiginomica+1 are real signals. But market depth is still insufficient to declare an "economy." |

"Every company needs an agent strategy" | Strong Support | Real enterprise adoption | Gartner: enterprise apps with AI agents will grow from 5% to 40% by end of 2026. UiPath: 77% of IT leaders have agentic AI investment plans. |

"AI agents will break seat-based pricing" | Partial Support | Mid-term real risk | If one agent does the work of 5–10 licenses, the pricing model must change. But this transition plays out over years — sudden collapse scenarios are overstated. |

3. Use Case Analysis

Use Case | Maturity | Commercial Potential | Key Barriers | Verdict |

|---|---|---|---|---|

Software Development | ⭐⭐⭐⭐⭐ High | ⭐⭐⭐⭐⭐ Very High | Hallucination, test reliability | Most mature. Cursor $1B ARR, GitHub Copilot 20M users. Agentic code review, test writing, and bug-fix loops in real production. |

Customer Service | ⭐⭐⭐⭐ Med-High | ⭐⭐⭐⭐⭐ Very High | Trust, hallucination, product complexity | Salesforce Agentforce's largest use case. Real enterprise deploys at Williams-Sonoma, SharkNinja. ROI is proven in this arena. |

Cybersecurity (SOC) | ⭐⭐⭐⭐ Med-High | ⭐⭐⭐⭐ High | False positives, accountability | CrowdStrike Charlotte AI, Palo Alto XSIAM in real production. Seven dedicated security agents active. Agentic SOC concept going mainstream. |

Finance / Back-Office | ⭐⭐⭐ Medium | ⭐⭐⭐⭐⭐ Very High | Regulation, GDPR, data sensitivity | IBM/Oracle partnership active for invoice, order, contract agents. High regulatory environment slows pace. |

Sales & CRM | ⭐⭐⭐ Medium | ⭐⭐⭐⭐ High | CRM data quality, integration complexity | Agentforce Sales at $2.3B. Amazon Bedrock-powered Rox platform reports 50% sales productivity gains. |

IT Operations | ⭐⭐⭐⭐ Med-High | ⭐⭐⭐⭐ High | Legacy system integration | ServiceNow delivers the strongest proof: 450K agents in its own operations, 80%+ automation. Rich ITSM automation opportunity. |

Research / Knowledge Work | ⭐⭐⭐ Medium | ⭐⭐⭐ Medium | Hallucination trust issue, verification need | Google Gemini Enterprise Deep Research agent, Anthropic Claude Cowork in early launch phase.pulsemcp+1 Still early-stage in enterprise knowledge work. |

RPA Intersection | ⭐⭐⭐⭐ High | ⭐⭐⭐⭐ High | Agentic addition complexity | UiPath Maestro orchestrates third-party agents. RPA + AI combination in real production. Enterprise customer base is concrete. |

Personal Assistant / Task Exec | ⭐⭐ Low-Med | ⭐⭐⭐ Medium | Security, access management, privacy | Anthropic Claude Cowork, Google Gemini Enterprise — recent launches. Enterprise context still being built. |

Supply Chain | ⭐⭐ Low-Med | ⭐⭐⭐⭐ High | Data integration, real-time reliability | Oracle SCM agents active but most still in early pilot. Wide-scale production 1–2 years away. |

4. Infrastructure Layer Analysis

The clearest and fastest value-creating layer of the AI agent trend is infrastructure. Applications are transforming, platforms are competing, but infrastructure grows under every scenario.

Compute and GPU Demand

Agentic AI deployments consume 20–30 times more tokens than standard generative AI usage. This signals that demand for GPU and inference infrastructure will grow disproportionately as the agent trend scales. Nvidia CEO Jensen Huang announced a $1 trillion revenue forecast through 2027, with inference demand as a primary driver.

Data and Orchestration Infrastructure

Agent systems require long-term data storage for memory, vector databases for semantic search, and workflow orchestration for multi-system actions. Snowflake, MongoDB, and Datadog are early-positioned platforms in this space. Cloudflare is attempting to build the "rails" of the agentic internet through MCP servers and distributed agent infrastructure.

Network Infrastructure

Low latency and high bandwidth are critical for AI clusters. Arista Networks announced a $105B AI networking TAM and doubled its 2026 AI networking revenue outlook. The 800G Ethernet transition is directly fed by AI workload requirements.

Security and Identity Layer

Autonomous AI agents taking actions create a new security and identity management layer. OWASP LLM Top 10 v2025 includes agent-specific threat categories. Reports indicate 82% of companies grant AI agents access to sensitive data with insufficient oversight. This opens a new addressable market for cybersecurity companies.

5. Public Company Impact Map

Company | Ticker | Impact Type | Direction | Mechanism | Horizon | Risk |

|---|---|---|---|---|---|---|

Nvidia | NVDA | Infra Winner | 🟢 Strong+ | Agentic AI 20-30x more inference tokens; all agent deployments depend on GPU infra; Blackwell GB200 $11B in Q1 | Short-Mid | Competition (AMD, custom chips); DeepSeek-style efficiency jumps |

AMD | AMD | Infra Winner | 🟡 Positive | MI300X as Nvidia alternative; hyperscalers want to avoid single-vendor dependency | Mid | Trails Nvidia software ecosystem (CUDA) |

Broadcom | AVGO | Infra Winner | 🟢 Strong+ | Custom ASIC chips (Google TPU, Meta chips); large share of hyperscaler capex; AI networking | Short-Mid | Hyperscaler customer concentration risk |

TSMC | TSM | Infra Winner | 🟢 Strong+ | Manufactures Nvidia Blackwell, Apple, AMD chips; AI chip demand feeds directly into capacity | Short-Mid | Geopolitical risk (Taiwan); US-China tensions |

Arista Networks | ANET | Infra Winner | 🟢 Strong+ | 800G Ethernet for AI cluster networking; $105B TAM; 2026 AI outlook doubled | Short-Mid | Cisco competition; hyperscalers building own network hardware |

Microsoft | MSFT | App Winner | 🟢 Strong+ | M365 Copilot 15M paid seats +160% YoY; GitHub Copilot 20M users; Azure AI full-stack; reach into every enterprise customer | Short-Mid | OpenAI independence risk; Copilot real revenue undisclosed |

Amazon (AWS) | AMZN | App Winner | 🟢 Strong+ | AWS Bedrock multi-billion ARR, customer spend +60% QoQfuturumgroup+1; Trainium2 inference cost advantage; $244B backlog | Short-Mid | Azure and Google Cloud competition |

Alphabet (Google) | GOOGL | App Winner | 🟡 Positive | Gemini Enterprise launch; Google Workspace agent integration; Vertex AI platform; but enterprise sales force weaker than Microsoft | Mid | OpenAI, Microsoft competition; ad revenue dilution risk |

Salesforce | CRM | App Winner + Risk | 🟡 Mixed | Agentforce $540M ARR +330% YoY; 18,500+ deals; but OpenAI agent platform is a direct competitor; SaaS model pressure | Mid | Agentforce cannibalization of core SaaS revenue; OpenAI Frontier competition |

ServiceNow | NOW | App Winner | 🟢 Strong+ | "Agentic enterprise OS" positioning; 1,000+ pre-built agents; IT/HR/CS workflow dominance; +21% subscription growth | Mid | Business model transition cost; cheaper rival agents |

UiPath | PATH | App Winner + Enabler | 🟡 Positive | RPA + AI agent integration; Maestro orchestration platform; agents embedded in existing robotic infrastructure | Mid | Microsoft Power Automate competition; standalone agent platforms |

CrowdStrike | CRWD | Enabler SW | 🟢 Strong+ | Charlotte AI with agentic SOCtradingview+1; both provides security and secures AI agents; most agentic security strategy among $100B+ market cap players | Mid | Unpredictable threat profiles from agent identity |

Palo Alto Networks | PANW | Enabler SW | 🟢 Positive | XSIAM AI-driven platform; agent security growing segment; strong SASE and platformization strategy | Mid | Intense competition with CrowdStrike |

Oracle | ORCL | Enabler SW | 🟡 Positive | Oracle AI Agent Marketplace with 100+ agents; Fusion Cloud embedded agents; IBM partnership | Mid | Legacy vendor perception; modernization pace |

IBM | IBM | Indirect Beneficiary | 🟡 Positive | watsonx Orchestrate multi-agent management; Oracle, Salesforce integrationsnewsroom.ibm+1; consulting services benefit from AI transformation | Mid-Long | Weak own software portfolio; pressure on service margins |

Accenture | ACN | Indirect Beneficiary | 🟡 Positive | AI Refinery platform; active on Oracle, Salesforce agent marketplacesaccenture+1; enterprise AI consulting revenue growing | Mid | AI automation can undermine the IT services business model itself |

Snowflake | SNOW | Enabler SW | 🟡 Positive | Cortex Agents, Snowflake Intelligence, vector storage; critical in agent system data layer; but growth deceleration risk | Mid | Databricks competition; hyperscaler native data services |

Datadog | DDOG | Enabler SW | 🟢 Positive | AI LLM observability, agent monitoring; agent systems require far more observability; multi-model tracking; cost monitoring | Short-Mid | Hyperscaler native monitoring competition |

MongoDB | MDB | Enabler SW | 🟡 Positive | Atlas Vector Search; agent memory and context storage; developer-native GenAI integration | Mid | Managed Postgres + pgvector, Pinecone competition |

Cloudflare | NET | Enabler SW | 🟢 Strong+ | MCP servers, agent runtime infrastructure; edge AI inference; 48% RPO growth; "rails of the agentic internet" | Short-Mid | Hyperscaler edge competition; revenue model maturity |

HubSpot | HUBS | Under Pressure | 🔴 Risk | OpenAI and general agent platforms can bypass CRM workflows; SMB-focused products are more vulnerable; per-seat pressure | Short-Mid | Lacks deep integrated data infrastructure of large enterprise apps |

Adobe | ADBE | Under Pressure | 🔴 Risk | Creative workflow democratization; Firefly is strong but Canva, Runway, AI-native alternatives apply pressure; shares down 44% from 52-week high | Short-Mid | High operating margin buffer; full displacement risk is low but pricing pressure is real |

6. Stock Baskets by Theme

🏗️ Infrastructure Winners

The most concrete and least contested revenue stream. This group grows regardless of which agent application wins.

- Nvidia (NVDA): Primary beneficiary of inference demand surge; Blackwell architecture; $1T revenue path

- Broadcom (AVGO): Custom AI ASIC chips; AI networking (VSP); large share of hyperscaler capex budgets

- TSMC (TSM): Manufactures all advanced-node AI chips; the physical fulfillment of AI demand

- Arista Networks (ANET): Setting the Ethernet standard for AI cluster networking; $105B TAM

- AMD (AMD): MI300X offers an alternative to Nvidia; hyperscaler competition drives this

🖥️ Enterprise Software Winners

Highest organic revenue growth potential from agent platformization.

- ServiceNow (NOW): Agentic enterprise OS positioning; IT/HR/CS workflow dominance; 1,000+ agents

- Salesforce (CRM): Agentforce $540M ARR, 330% growth; 18,500+ deals; both winner and risk

- Microsoft (MSFT): Full stack in M365 + GitHub + Azure; Copilot fastest-growing M365 product

- Amazon / AWS (AMZN): Bedrock, Trainium, $244B backlog; enterprise AI stack dominance

- Oracle (ORCL): Fusion ERP + AI Agent Marketplace; difficult but critical enterprise data ownership

⚙️ Workflow / Automation Winners

- UiPath (PATH): RPA roots + AI agent orchestration; Maestro platform; 90% of IT execs cite improvement

- ServiceNow (NOW): Featured again — its workflow framework is the enterprise platform most ready for the agent layer

- Cloudflare (NET): MCP server infrastructure; edge agent runtime and routing

⚠️ SaaS Players Under Pressure

- Adobe (ADBE): Creative workflow democratization; high margin buffer exists but pricing pressure is real

- HubSpot (HUBS): SMB CRM agent bypass risk; per-seat pressure

- Atlassian (TEAM): Software development tools changing with AI; but project management complexity provides protection

- Zendesk / Freshworks: Customer service agents are both a threat and opportunity for these players

🔍 Speculative Candidates to Watch

- Cursor (private, not public): $1B ARR, $29.3B valuation — IPO watchlist candidate

- Datadog (DDOG): AI observability is a strong theme; but valuation already premium

- MongoDB (MDB): Atlas Vector Search + agentic memory; developer-native positioning

- Snowflake (SNOW): Cortex Agents + enterprise data partnerships; consumption growth is the critical metric

- Palo Alto Networks (PANW): Direct beneficiary if agentic security standards solidify

7. Critical Disruption Risks

Technical Risks

- Hallucination problem: Various studies indicate that fewer than 20% of LLM responses are accurate enough for enterprise decision-making. In multi-agent systems, these risks compound on top of one another.

- Token cost explosion: Agentic AI consumes 20–30x more tokens than standard AI. Gartner forecasts that more than 40% of projects will be canceled by 2027 due to high infrastructure costs.

- Latency and reliability: Multi-agent systems can cost 5–10x more than single-agent systems. Response time variability conflicts with enterprise SLAs.

- Integration brittleness: 86% of enterprises reportedly require infrastructure upgrades before full deployment. State management failures account for 40% of agent failures.

Cost Risk

- Initial deployment cost for a mid-size enterprise agent ranges from $50,000–$200,000. Hidden costs (integration, maintenance, training) can add 30–60% to the first-year budget. Operating costs reportedly represent 65–75% of total cost of ownership.

Regulatory and Trust Risk

- The EU AI Act entered into force in 2024; obligations for high-risk systems phase in through 2026. Agent deployment in finance, healthcare, and hiring requires serious compliance work.

- 57% of companies report an average financial loss of $4.4M from AI-related incidents. Autonomous action-taking capability multiplies audit and accountability challenges compared to standard LLM use.

Enterprise Adoption Risk

- Deloitte research shows 60% of organizations cite legacy integration and risk/compliance concerns as primary barriers. Data privacy (53%), integration complexity (40%), and high cost (39%) are the top three barriers.

- Full enterprise change management takes 1–2 years even after a 3–6 month production runway. The "fast pilot, slow scale" pattern remains the dominant adoption cycle.

Competition and Commoditization Risk

- "Agent washing": Beyond the ~130 truly agentic providers, most of the market is rebranded chatbots. Which players will be real winners remains unclear.

- The model layer is commoditizing rapidly. OpenAI GPT-5, Gemini 2.5, and Claude 3.7 competition is squeezing model margins. Real value will accumulate in orchestration, data, and integration layers.

- OpenAI's "Frontier" platform directly threatens Salesforce, Workday, and Adobe — the real scale is debatable, but the market is already repricing.

8. Closing Thesis: Where Is the Real Money in AI Agents?

Real money in the AI agent narrative is accumulating in at least three distinct layers that will continue to compound: first, in compute and inference infrastructure — Nvidia, Broadcom, and TSMC collect payment under every scenario because agents consume more GPU time; second, in orchestration and workflow platforms — ServiceNow and UiPath, which hold the bridge to enterprise processes, are positioned to impose their frameworks on incoming agents; third, in software development tooling — Cursor's $1B ARR in 24 months proves that developer tooling is the first area where humans are willing to pay real money for genuine agent value. The intersection of risk capital, revenue growth, and enterprise commitment in these three layers represents the clearest investor positioning. SaaS disruption is real but long-cycle and selective; unlike infrastructure companies, application software players must simultaneously fight opportunity and threat. That distinction will define which stocks deserve premium valuation and which do not.