Why Real World Assets Are Becoming Crypto’s Next Major Narrative

For most of crypto’s history, the industry operated largely inside its own financial sandbox.

DeFi protocols traded synthetic assets. Stablecoins moved liquidity between exchanges. Yield farming revolved around crypto-native collateral.

But over the past two years, a new narrative has steadily gained momentum: Real World Assets (RWA).

The core idea behind RWA is simple but powerful.

Instead of building financial markets exclusively around crypto-native assets, blockchain infrastructure can be used to represent traditional financial instruments directly on-chain.

These assets can include:

- U.S. Treasury bills

- money market funds

- equities and ETFs

- private credit

- commodities such as gold

- real estate-backed securities

Once tokenized, these assets can move through blockchain networks just like cryptocurrencies. They can be traded, used as collateral, integrated into DeFi, or distributed globally.

In theory, tokenization transforms traditional finance from a closed institutional system into an open programmable financial network.

And according to the latest data, this transformation is already underway.

The Current State of the RWA Market

While the RWA narrative is often discussed in abstract terms, the market itself has begun to generate meaningful scale.

According to data from DeFiLlama, the total value of tokenized real-world assets has reached approximately $22.2 billion.

Within this broader category, several segments have emerged as clear leaders.

Tokenized U.S. Treasuries currently represent the largest share of growth. These products allow investors to gain exposure to short-term government debt through blockchain-based tokens.

Tokenized stocks and ETFs are another rapidly expanding segment. The market for tokenized equities has already reached roughly $1.2 billion, and interest continues to accelerate.

Beyond those two categories, private credit and structured credit products are increasingly moving on-chain as well.

Together, these segments represent the early stages of a much larger structural shift.

For decades, financial markets have relied on centralized clearing houses, custodians, and intermediaries to manage asset ownership and settlement.

Tokenization offers a fundamentally different model.

Instead of relying on traditional financial rails, ownership and settlement can be managed directly on blockchains.

A Shift from Crypto Narrative to Institutional Infrastructure

For years, RWA discussions were largely theoretical.

Many observers believed tokenization would eventually happen, but real institutional adoption seemed distant.

That perception has changed rapidly over the past year.

Several developments suggest that the RWA narrative is moving from speculation toward real financial infrastructure.

For example, recent reports from Nasdaq indicate that the exchange operator has been exploring tokenization infrastructure partnerships with Kraken.

The goal of these collaborations is to develop systems capable of supporting tokenized securities trading.

At the same time, U.S. banking regulators have signaled that tokenized securities will not necessarily face additional capital penalties.

This regulatory clarity is important.

Financial institutions often avoid emerging technologies until regulatory treatment becomes predictable.

The absence of additional capital requirements significantly lowers the barrier to experimentation.

Together, these developments point to a broader conclusion.

The RWA narrative is no longer just a crypto-native theme.

It is becoming a potential bridge between traditional capital markets and blockchain infrastructure.

What Is Actually Growing Inside the RWA Ecosystem?

One of the challenges when discussing RWAs is that the term encompasses many different types of assets.

Not all tokenized assets behave the same way.

In reality, the RWA ecosystem can be divided into several distinct sub-sectors.

Understanding these segments is critical for investors trying to identify where growth is actually occurring.

Tokenized Treasuries and Money Market Funds

Tokenized U.S. Treasuries are currently the most mature segment of the RWA market.

The appeal is straightforward.

U.S. Treasury bills provide relatively low-risk yield backed by the U.S. government.

By tokenizing these instruments, financial institutions can offer blockchain-based products that combine traditional fixed income exposure with on-chain settlement.

This has proven particularly attractive during periods of elevated interest rates.

Instead of earning near-zero yields in stablecoins, investors can gain exposure to real-world government bond yields while remaining inside the crypto ecosystem.

Several protocols have launched tokenized treasury products that allow these instruments to circulate across blockchain networks.

As a result, tokenized government debt has become the largest and fastest growing RWA category.

Tokenized Stocks and ETFs

Another rapidly emerging category is tokenized equities.

The concept here is simple.

Traditional stocks can be represented as blockchain tokens that track the underlying asset.

This allows users to gain exposure to equity markets while interacting directly with blockchain infrastructure.

Tokenized stocks could eventually enable several advantages:

- global 24/7 trading

- programmable financial instruments

- seamless integration with DeFi protocols

- fractional ownership structures

Although this market remains relatively small today, it is growing quickly as exchanges and fintech platforms explore new tokenization models.

Private Credit and Structured Finance

A less visible but highly important segment of the RWA ecosystem is private credit.

Private credit refers to loans originated outside traditional public bond markets.

These loans can include:

- corporate financing

- asset-backed lending

- trade finance

- infrastructure financing

Blockchain infrastructure can provide transparency and distribution advantages for these products.

Instead of relying solely on private institutional networks, tokenized credit instruments can potentially be distributed to a broader investor base.

Protocols focused on structured credit tokenization have begun experimenting with these models.

While still early, this category could eventually represent a large portion of the RWA ecosystem.

Commodities and Tokenized Gold

Tokenized commodities represent another niche within the RWA sector.

Gold-backed tokens, in particular, have gained traction among investors seeking exposure to physical bullion without managing custody themselves.

These tokens function as digital representations of vaulted gold reserves.

Unlike many RWA projects, commodity tokens often behave more like digital asset wrappers rather than infrastructure protocols.

Their value derives directly from the underlying asset rather than network growth.

The Infrastructure Layer Beneath RWA

While tokenized assets attract most of the attention, the infrastructure required to support them is equally important.

A functioning RWA ecosystem requires several layers of infrastructure working together.

These include:

- price oracle networks

- compliance and identity systems

- asset issuance platforms

- distribution networks

- cross-chain messaging infrastructure

Without these components, tokenized assets cannot scale beyond small pilot programs.

This is why many investors are focusing not only on asset issuers but also on infrastructure providers.

Infrastructure tends to capture value across multiple asset categories.

If tokenization expands broadly across financial markets, the protocols powering these systems could become extremely valuable.

Which Crypto Projects Benefit from the RWA Narrative?

With that context in mind, investors often ask a straightforward question.

If real-world assets move on-chain, which crypto networks benefit the most?

The answer is not limited to a single category.

Different types of projects capture value from different parts of the tokenization stack.

Broadly speaking, the beneficiaries fall into several groups.

Direct RWA Asset Platforms

These projects focus directly on issuing or distributing tokenized assets.

Ondo Finance

Among RWA-focused projects, Ondo has become one of the most prominent.

The protocol specializes in bringing traditional financial yield products onto blockchain networks.

Data from DeFiLlama shows that Ondo’s yield-bearing assets have reached more than $2 billion in total value locked.

This reflects growing demand for tokenized treasury exposure within the crypto ecosystem.

Ondo’s strategy focuses on two major areas:

- tokenized U.S. Treasuries

- tokenized equities

Because the narrative around Ondo is extremely straightforward, it has become one of the most recognizable ticker symbols associated with the RWA theme.

Markets tend to favor narratives that can be explained quickly.

Ondo fits that pattern well.

Centrifuge

Centrifuge represents a different approach to the RWA ecosystem.

Instead of focusing on treasury products, the protocol specializes in private credit tokenization and institutional asset financing.

Through partnerships with asset managers and lending platforms, Centrifuge enables real-world loan portfolios to be tokenized and distributed across DeFi systems.

Recent developments have demonstrated how these tokenized assets can integrate directly with DeFi lending protocols.

In some cases, tokenized credit instruments have even been used as collateral inside lending markets.

This type of composability highlights the long-term potential of RWA infrastructure.

Infrastructure Winners: The “Picks and Shovels”

If tokenized assets represent the visible part of the RWA market, infrastructure providers represent the foundation underneath.

Among these infrastructure projects, one network continues to stand out.

Chainlink

Chainlink may be one of the most important infrastructure projects supporting the RWA ecosystem.

Tokenizing assets alone is not enough.

Financial systems require several additional components:

- accurate pricing data

- proof of reserve verification

- market data feeds

- cross-chain communication

Chainlink’s product suite directly addresses these needs.

The network already provides:

- oracle price feeds

- Proof of Reserve systems

- low-latency data streams

- cross-chain messaging through CCIP

Because of this, Chainlink is often described as the data infrastructure layer for tokenized finance.

If RWA markets expand significantly, the demand for reliable financial data infrastructure will likely grow alongside them.

This makes Chainlink one of the most widely discussed infrastructure bets within the RWA narrative.

RWA-Focused Networks

Beyond asset issuers and infrastructure providers, some blockchain networks are positioning themselves specifically as RWA-friendly ecosystems.

These networks aim to provide compliant environments where institutions can issue tokenized assets.

MANTRA

MANTRA is building a blockchain designed specifically for tokenized financial assets.

The network emphasizes regulatory compliance and institutional integrations.

Partnerships with cloud providers and enterprise infrastructure platforms are intended to support this positioning.

However, MANTRA has also faced questions around token distribution and ecosystem trust.

For investors, this creates a classic high-risk, high-reward dynamic.

If execution succeeds, the network could capture a large share of RWA issuance.

But the risks surrounding governance and adoption remain meaningful.

Stellar

Stellar represents a more understated participant in the RWA ecosystem.

While it rarely appears in speculative narratives, Stellar has long focused on compliant financial infrastructure.

The network has been used for:

- payment settlement systems

- tokenized asset issuance

- cross-border financial transfers

Several institutions experimenting with tokenized assets have explored Stellar as a distribution rail.

If tokenized assets begin prioritizing real-world settlement and payment integration, networks like Stellar could benefit indirectly.

Ethereum

Although Ethereum is not typically described as an “RWA coin,” it remains one of the most important settlement layers for tokenized assets.

Many institutional tokenization experiments still rely on Ethereum or EVM-compatible environments.

If large-scale financial tokenization occurs, a significant portion of that activity may ultimately settle on Ethereum infrastructure.

For this reason, Ethereum represents a foundational but indirect beneficiary of the RWA trend.

Early Conclusion

The RWA narrative is evolving quickly.

What began as a theoretical concept is gradually transforming into a real financial infrastructure experiment.

Several segments are already showing strong growth:

- tokenized U.S. Treasuries

- tokenized equities

- private credit markets

Around these assets, a complex infrastructure stack is emerging.

Some projects focus on issuing tokenized assets.

Others provide the underlying infrastructure required to make these systems work.

From an investment perspective, the RWA ecosystem can be divided into several strategic categories:

Direct asset platforms

Infrastructure providers

RWA-focused blockchain networks

Understanding these distinctions helps clarify where value may ultimately accrue as tokenization expands.

Investment Landscape, Coin Analysis, and the Future of Tokenized Markets

In Part 1, we explored the structural foundation of the real-world asset (RWA) narrative: the growth of tokenized treasuries, equities, private credit markets, and the infrastructure required to bring traditional finance on-chain.

But narratives alone do not drive markets.

For investors, the key question is simpler:

If RWA adoption accelerates, which crypto assets actually capture the value?

The answer depends on where each project sits in the tokenization stack.

Some protocols issue the assets themselves.

Others provide financial infrastructure.

And some operate the blockchain rails that settlement occurs on.

Understanding these categories is essential for identifying which tokens might benefit most from the expansion of tokenized finance.

The RWA Investment Stack

A useful way to analyze the ecosystem is to divide projects into four strategic layers.

Asset Issuers

Protocols that directly tokenize real-world assets and distribute them on-chain.

Infrastructure Providers

Networks that provide pricing data, compliance tools, or interoperability layers required for tokenized assets to function.

Tokenization Networks

Blockchains designed to host regulated financial assets.

Settlement Layers

Major smart contract platforms where tokenized assets ultimately live and settle.

Each category captures value in different ways.

Asset issuers benefit from product demand.

Infrastructure providers benefit from network usage across many assets.

Settlement layers benefit from transaction volume and ecosystem gravity.

With that framework in mind, we can examine the projects most closely associated with the RWA narrative.

Tier 1: Core RWA Exposure

These projects represent the most direct exposure to the tokenization theme.

They are often the first assets investors examine when the RWA narrative gains momentum.

Ondo Finance

Among all RWA projects, Ondo is arguably the clearest narrative play.

The protocol focuses on bringing traditional yield-bearing assets — particularly U.S. Treasury exposure — onto blockchain networks.

Its products are designed to bridge institutional finance and DeFi markets.

Rather than offering purely crypto-native yield strategies, Ondo provides exposure to traditional financial instruments packaged in tokenized form.

This positioning has made the protocol one of the fastest growing participants in the RWA sector.

According to data from DeFiLlama, Ondo’s ecosystem has surpassed $2 billion in total value locked, driven primarily by demand for tokenized treasury products.

From a narrative standpoint, Ondo has a major advantage.

Its story is extremely simple:

Tokenized government bonds on blockchain rails.

Markets tend to reward projects with narratives that are easy to explain.

In many ways, Ondo has become the purest “RWA theme” asset in the market today.

However, simplicity does not eliminate risk.

The long-term value of the token ultimately depends on whether tokenized treasury products scale beyond early crypto-native demand.

If traditional institutions adopt these structures, Ondo could benefit significantly.

But if the market remains limited to crypto-native investors seeking yield alternatives, growth may be slower than expected.

Centrifuge

Centrifuge represents a different part of the tokenization ecosystem.

Instead of focusing on treasury products, the protocol specializes in private credit and structured finance.

Private credit markets are massive.

Globally, private lending has grown into a multi-trillion-dollar industry as banks reduce balance sheet lending and institutional investors search for higher yield opportunities.

Centrifuge’s goal is to bring these credit markets on-chain.

The protocol allows real-world loan portfolios to be tokenized and financed through blockchain infrastructure.

Recent integrations have demonstrated how these assets can interact with DeFi lending markets, creating new forms of capital efficiency.

In some cases, tokenized credit instruments have even been used as collateral in decentralized lending protocols.

This creates an interesting feedback loop:

Traditional financial assets provide yield, while DeFi protocols provide liquidity and distribution.

If this model proves scalable, Centrifuge could become a key infrastructure layer for on-chain credit markets.

However, the complexity of private credit also introduces risk.

Unlike government bonds or publicly traded equities, credit portfolios require extensive due diligence and risk management.

Scaling these markets on-chain will require both technological infrastructure and strong institutional partnerships.

Tier 1 Infrastructure: The Picks-and-Shovels Layer

While asset issuers attract attention, infrastructure providers often capture value across the entire ecosystem.

If tokenization expands across multiple asset categories, infrastructure networks could benefit regardless of which issuer dominates.

Chainlink

Within the RWA ecosystem, Chainlink occupies a unique role.

Tokenized assets cannot function without reliable financial data.

When traditional assets move on-chain, several critical problems emerge immediately.

Smart contracts must know the correct price of an asset.

Investors must verify that reserves exist.

Financial data must update quickly enough to support trading and lending markets.

Assets may also need to move between multiple blockchain networks.

Chainlink’s infrastructure addresses each of these challenges.

The network provides:

price oracle feeds

proof-of-reserve verification

low-latency financial data streams

cross-chain messaging infrastructure

This makes Chainlink one of the most important picks-and-shovels infrastructure providers in the tokenization ecosystem.

If RWA markets expand dramatically, the demand for reliable oracle infrastructure will likely increase alongside them.

In this sense, Chainlink represents a different type of investment thesis.

Rather than betting on a specific tokenized asset category, investors are betting on the data infrastructure required to support the entire market.

Historically, infrastructure providers often capture significant value during technological transitions.

In traditional markets, companies that provide core financial infrastructure — exchanges, data providers, clearing systems — often become extremely valuable over time.

Chainlink’s long-term thesis resembles that model.

Tier 2: Higher-Beta RWA Narratives

Beyond the established infrastructure and asset issuance platforms, several newer projects are attempting to build entire blockchain ecosystems around tokenized finance.

These projects often carry higher upside potential, but they also face greater execution risk.

MANTRA

MANTRA positions itself as a blockchain specifically designed for tokenized financial assets.

The network emphasizes regulatory compliance, identity systems, and institutional integration.

This positioning reflects a growing belief among some investors that traditional institutions may prefer purpose-built financial blockchains rather than general-purpose smart contract platforms.

MANTRA’s partnerships with enterprise technology providers help reinforce this narrative.

However, projects attempting to build entirely new financial ecosystems face a difficult challenge.

They must attract both:

institutional asset issuers

and

liquidity providers

Without both sides of that equation, tokenization platforms struggle to generate meaningful activity.

For investors, this creates a classic high-beta trade.

If the network successfully attracts institutional adoption, the upside could be significant.

But execution risk remains substantial.

Plume Network

Plume represents another emerging RWA-focused ecosystem.

The project is building a blockchain environment specifically optimized for real-world asset issuance and distribution.

Compared to more established infrastructure projects, Plume remains early in its development cycle.

However, the narrative surrounding RWA-native blockchains has attracted speculative attention from investors seeking early exposure to tokenization infrastructure.

For now, Plume should be viewed primarily as a high-beta narrative asset.

Its long-term success will depend on whether the network can attract meaningful institutional partnerships and real asset issuance.

Tier 3: Indirect Beneficiaries

Not every beneficiary of the RWA trend will be a specialized tokenization platform.

Some of the biggest winners may actually be the existing blockchains where tokenized assets ultimately settle.

Ethereum

Ethereum remains the largest smart contract ecosystem in crypto.

Many institutional experiments with tokenized assets continue to rely on Ethereum or EVM-compatible networks.

Several factors explain this preference.

Ethereum provides:

a mature developer ecosystem

deep liquidity pools

battle-tested smart contract infrastructure

global distribution across exchanges and custodians

Even if specialized tokenization networks emerge, a significant portion of financial assets may still settle on Ethereum infrastructure.

For this reason, Ethereum represents one of the most important indirect beneficiaries of the RWA trend.

Stellar

Stellar occupies a different niche within the blockchain ecosystem.

The network has long focused on financial infrastructure such as cross-border payments and compliant asset issuance.

Several institutions experimenting with tokenized assets have explored Stellar as a distribution network for financial products.

Unlike many DeFi platforms, Stellar emphasizes regulatory compatibility and payment settlement infrastructure.

If tokenized assets begin prioritizing real-world distribution and payment functionality, networks like Stellar could play a larger role than many investors currently expect.

Comparing the RWA Investment Landscape

When viewed together, the RWA ecosystem reveals several distinct investment profiles.

Some tokens provide direct exposure to tokenized assets.

Others represent infrastructure required for the ecosystem to function.

And some represent blockchain networks where tokenized assets may ultimately live.

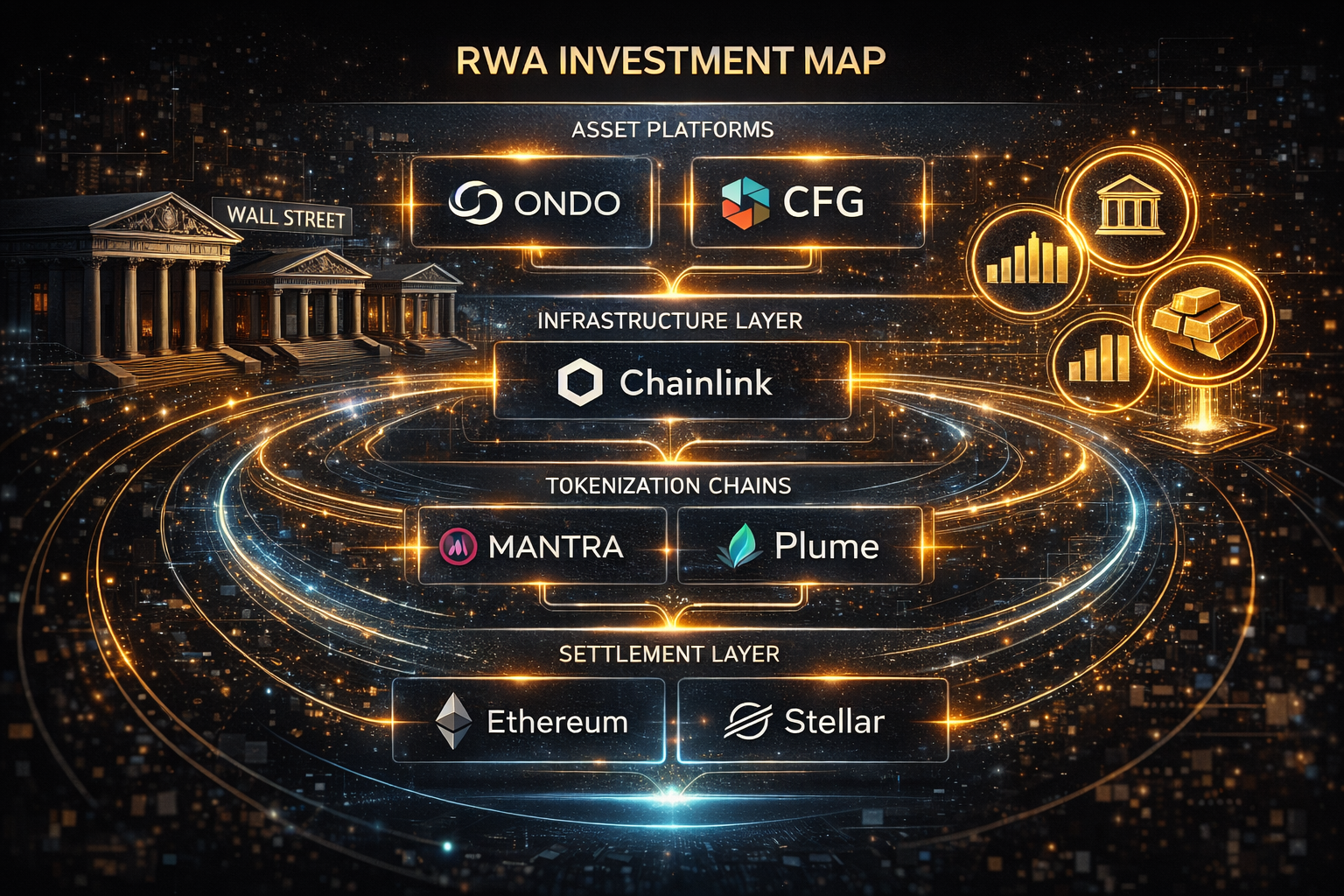

A simplified mental model might look like this:

Core RWA asset platforms

ONDO, CFG

Infrastructure layer

LINK

High-beta tokenization ecosystems

OM, PLUME

Settlement and distribution networks

ETH, XLM

Each category carries different risk and return characteristics.

Asset issuers may benefit quickly from narrative-driven capital flows.

Infrastructure providers may benefit more gradually as the ecosystem expands.

Settlement networks benefit from long-term structural adoption.

Public Market Winners of the RWA Trend

While most discussions around real-world asset tokenization focus on crypto protocols, the shift toward tokenized finance could also impact several publicly traded financial infrastructure companies.

If capital markets gradually move toward blockchain-based settlement and tokenized securities, the biggest winners may not only be crypto networks — but also companies providing the rails of global finance.

These companies generally fall into three categories:

- exchange infrastructure

- market data and financial infrastructure

- institutional crypto custody and tokenization services

Understanding this broader landscape helps place the RWA narrative in a much larger context.

Instead of being purely a crypto phenomenon, tokenization may ultimately reshape how global capital markets operate.

Exchange Infrastructure

Nasdaq

Nasdaq has already begun exploring tokenization infrastructure partnerships with crypto-native companies.

Reports suggest the exchange operator has explored systems capable of supporting tokenized securities trading infrastructure, including collaboration discussions with crypto platforms such as Kraken.

Nasdaq has long operated one of the world’s largest market technology businesses, providing trading infrastructure to dozens of exchanges globally.

If tokenized securities markets grow, Nasdaq could become a major provider of the technology layer connecting traditional exchanges with blockchain settlement systems.

Rather than replacing exchanges, tokenization may transform them into hybrid markets combining traditional market structure with blockchain-based settlement.

Financial Market Infrastructure

Intercontinental Exchange (ICE)

Intercontinental Exchange, the parent company of the New York Stock Exchange, operates some of the most important financial infrastructure in global markets.

Its ecosystem includes:

- the NYSE exchange

- derivatives trading venues

- fixed income markets

- financial data services

Historically, financial market transformations have consistently increased the value of data infrastructure providers.

If tokenized assets begin trading across blockchain networks, reliable pricing data and financial analytics will become even more important.

Companies like ICE could therefore play a central role in providing the data layer for hybrid tokenized markets.

Institutional Crypto Infrastructure

Coinbase

Among publicly traded companies, Coinbase may be one of the most direct beneficiaries of the RWA trend.

The company has increasingly positioned itself as institutional crypto infrastructure, offering services such as:

- institutional custody

- token issuance infrastructure

- stablecoin settlement rails

- blockchain market access for financial institutions

If tokenized securities become widely adopted, institutions will require secure custody solutions capable of holding both traditional assets and blockchain-based tokens.

Coinbase is actively building the infrastructure required to support this transition.

Asset Managers Entering Tokenization

BlackRock

Large asset managers are also beginning to explore tokenization.

BlackRock, the world’s largest asset manager, has already launched tokenized treasury products and continues experimenting with blockchain-based financial infrastructure.

For asset managers, tokenization could unlock several advantages:

- faster settlement

- programmable financial products

- global distribution of funds

- lower operational costs

If these benefits materialize, asset managers could eventually distribute investment products directly through blockchain networks.

The Hybrid Financial Future

The most likely outcome for tokenized finance is not a world where crypto replaces traditional markets entirely.

Instead, the future may resemble a hybrid financial system.

In this system:

- crypto networks provide programmable infrastructure

- traditional institutions provide market structure and liquidity

- investors interact with both environments simultaneously

This convergence between blockchain technology and traditional financial infrastructure is one of the key reasons the RWA narrative has gained so much attention.

It represents one of the first credible paths for Wall Street and crypto infrastructure to integrate.

The Biggest Risks to the RWA Thesis

Despite the excitement surrounding tokenization, the RWA narrative is not without risks.

One of the most important challenges is liquidity.

Tokenizing an asset does not automatically create a liquid market.

Many tokenized financial products remain relatively thinly traded compared to their traditional counterparts.

Another challenge involves regulation.

Financial markets operate under complex regulatory frameworks that vary across jurisdictions.

While regulators have shown increasing openness toward tokenization, global regulatory alignment remains uncertain.

There is also the question of token value capture.

In some cases, tokenized asset platforms generate economic activity without necessarily transferring that value to the protocol’s token.

This dynamic has already appeared in parts of the DeFi ecosystem.

For investors, distinguishing between protocol usage and token value capture will remain an important analytical challenge.

RWA Investment Map

Core RWA Exposure

ONDO

CFG

Infrastructure

LINK

High Beta

OM

PLUME

Settlement

ETH

XLM

Public Market Exposure

COIN

NDAQ

ICE

BLK

Final Thoughts

The RWA narrative represents one of the most significant structural shifts in financial infrastructure since the emergence of decentralized finance.

For most of crypto’s history, blockchain systems operated largely in isolation from traditional capital markets. DeFi protocols built financial products using crypto-native collateral, while traditional financial institutions continued operating on legacy settlement rails.

Real-world asset tokenization is beginning to change that dynamic.

Instead of existing as separate financial systems, blockchain infrastructure and traditional markets are gradually starting to converge.

Tokenized U.S. Treasuries, equities, and private credit instruments are already gaining traction across both crypto platforms and institutional experiments.

Around these assets, an entirely new financial stack is emerging.

Some projects focus on issuing tokenized assets directly on-chain.

Others provide the critical infrastructure required to support those assets — including oracle networks, compliance systems, custody platforms, and cross-chain messaging.

At the same time, traditional financial institutions and publicly traded companies are beginning to position themselves within this emerging ecosystem.

Exchanges such as Nasdaq, financial infrastructure providers like ICE, institutional crypto platforms such as Coinbase, and asset managers like BlackRock are all exploring how tokenization may reshape capital markets.

In other words, the RWA narrative is no longer just about crypto.

It represents a potential convergence between blockchain infrastructure and the existing global financial system.

If tokenization continues to expand over the coming decade, the winners may emerge across both worlds.

Crypto protocols may power the programmable infrastructure layer.

Traditional institutions may continue to provide liquidity, market structure, and asset distribution.

For investors, the challenge will not simply be identifying the next speculative token.

Instead, the key question will be much larger:

Which networks and institutions will become indispensable infrastructure in a tokenized financial system?

Because in the early stages of technological transformation, narratives dominate.

But over time, the most valuable platforms tend to be the ones that quietly become essential financial infrastructure.

And in the emerging world of tokenized finance, the race to build that infrastructure has only just begun.